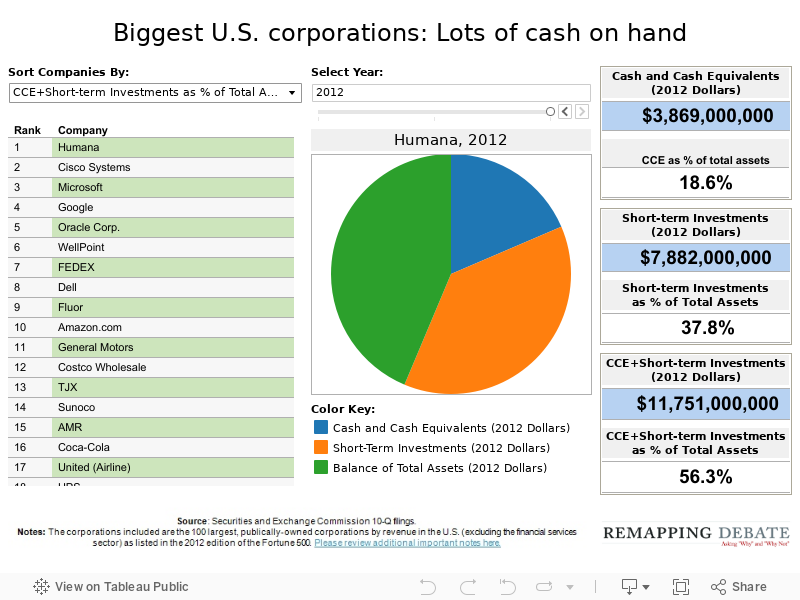

Sept. 26, 2012 — So how much pump-priming could America’s largest corporations achieve if they were to dig into their cash and cash equivalents as well as their short-term investments? Remapping Debate examined the relevant quarterly Securities and Exchange Commission filings of the 100 largest corporations by revenue as ranked by the Fortune 500 in 2012 (looking only at publicly-held corporations, and excluding those in the financial sector). We looked at filing data for the period closest to June 30th in 2012, 2006, and 2000.

The results are available to you in the data viz below, with each of three numbers calculated as a percentage of total assets for each of the three years: cash and cash equivalents (CCE) separately, short-term investments separately, and CCE and short-term investments combined (for 10 companies in 2000, comparable data were not available).

It turns out that more than 70 percent of the corporations listed in both 2012 and 2000 showed an increase over time in CCE and short-term investments combined as a percentage of total assets, including 15 corporations where the percentage point increase was 10 points or more.

The viz allows you to sort companies by their relative Fortune 500 rank; by the dollar amount of their CCE, short-term investments, or CCE and short-term investments combined; and by the percentage of total assets represented by CCE, short-term investments, or CCE and short-term investments combined. All figures have been inflation-adjusted to 2012 dollars.

You can also switch between a 2012, 2006, and 2000 view.

Important wrinkle in respect to Caterpillar, International Paper, Kroger, Target, and Valero: in one or more years, one or more of these companies did not disaggregate their CCE amount from their short-term investment amount. In each such case, we attributed all of the non-differentiated amount to CCE (thereby likely overstating CCE and understating short-term investments). In each affected year, short-term investments are listed as “not available” (and are reflected on the pie chart as an undifferentiated portion of CCE). For the short-term investment sorts, affected companies are listed at the bottom. For CCE sorts, however, the affected companies are listed as they would be if all CCE and short-term investments were properly attributed to CCE, thereby potentially skewing the rankings. This issue has no impact on the rankings for CCE and short-term investments combined.

Note: when you change views, neither the pie chart nor the dollar and percentage values change to the first-listed company; you must manually click on a company name to refresh the data. Please also review these important notes.