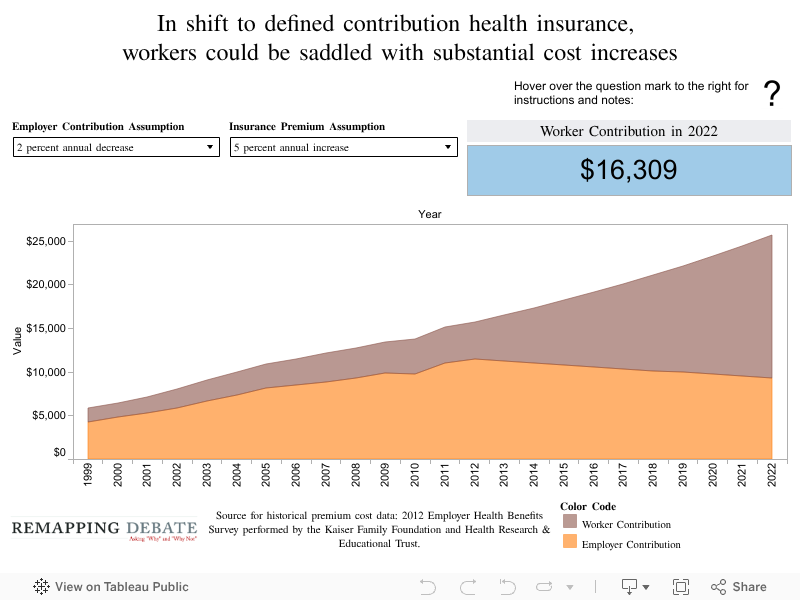

Oct. 24, 2012 — As explained in the accompanying article, the main reason motivating an employer to move to a defined contribution system is to reduce its own cost curve for employee benefits below that of the annual increases in health care premiums, leaving employees to pay more of the bill.

How much more will depend on two variables: the extent to which health insurance premiums increase over time and the decisions employers make to adjust their contributions. This visualization allows you to see how much of a gap the employee will have to fill under a variety of scenarios. Use the filters at the top to choose different annual rate changes in average health insurance premium cost and in employer contribution.

Contribution scenarios range from lowering contributions by 2 percent each year (a continuation of the same cost cutting impulse that gave rise to the shift to defined contribution in the first place), to keeping contributions flat, to raising contributions by 2 percent per year (most experts do not expect a company to increase its contribution at a rate greater than the increase in overall compensation, which has been running at about 1 to 2 percent per year).

Premium increase scenarios range from 5 to 9 percent (premiums have increased at an average rate of about 7 percent a year for the last decade. Most analysts expect that premiums will continue to increase by at least 5 percent a year into the foreseeable future, despite the cost control mechanisms included in the health reform law; some industry experts expect even higher increases of about 9 percent).

Note: this visualization presumes that an employee continues to have available, and chooses to select, an equivalent health plan to what he has had. Many cost control advocates would argue that employees will wind up having less of a gap to pay for than shown in the visualization because they will have had a “light bulb moment” and will decide to “chose” inferior coverage.